Why Wall Street Banks Can't Handle The Truth

Over the past 12 years, longtime banking analyst Mike Mayo has issued numerous calls to sell bank stocks, a rarity in a system where nearly all stocks are rated buy or hold. His negative ratings have frequently gotten him in trouble with banks, clients and his own bosses, who didn't want to alienate those companies. In this excerpt from his new book, "Exile on Wall Street," Mr. Mayo gives an inside view of the fights, the scolding and the threatening phone calls he received as a result of yelling "sell"—and offers a proposal to fix the banking sector.

By Mike Mayo

Taking a negative position doesn't win you many friends in the banking sector. I've worked as a bank analyst for the past 20 years, where my job is to study publicly traded financial firms and decide which ones would make the best investments. This research goes out to institutional investors: mutual fund companies, university endowments, public-employee retirement funds, hedge funds, and other organizations with large amounts of money. But for about the past decade, especially the past five years or so, most big banks haven't been good investments. In fact, they've been terrible investments, down 50%, 60%, 70% or more.

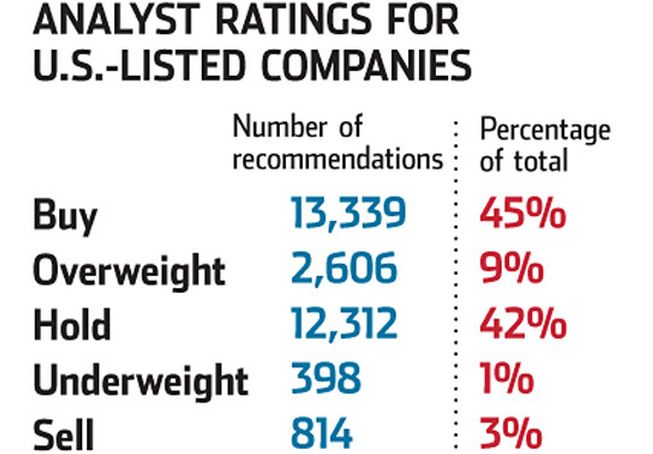

Analysts are supposed to be a check on the financial system—people who can wade through a company's financials and tell investors what's really going on. There are about 5,000 so-called sell-side analysts, about 5% of whom track the financial sector, serving as watchdogs over U.S. companies with combined market value of more than $15 trillion.

Unfortunately, some are little more than cheerleaders—afraid of rocking the boat at their firms, afraid of alienating the companies they cover and drawing the wrath of their superiors. The proportion of sell ratings on Wall Street remains under 5%, even today, despite the fact that any first-year MBA student can tell you that 95% of the stocks cannot be winners.

Over the years, I have pointed out certain problems in the banking sector—things like excessive risk, outsized compensation for bankers, more aggressive lending—and as a result been yelled at, conspicuously ignored, threatened with legal action and mocked by banking executives, all with the intent of persuading me to soften my stance.

Looking inside the world of finance—with its pressures to conform and stay quiet—may offer some insight into why so many others have fudged. And it may offer some answers as to how crisis after crisis has hit the economy over the past decade, taking the markets by surprise, despite what should have been plentiful warning signs.

***

It started in 1999, when I was managing director (the equivalent of partner) at Credit Suisse First Boston. At the time, what gave me the biggest concern was a sense that stocks within the banking sector were likely to turn downward.

Five years after the interstate banking law of 1994, which allowed banks to operate across state lines, the easy gains from consolidation were over. When banks couldn't maintain their growth momentum through mergers and cost cuts, they took the next logical step—they made more consumer loans. Logic dictated that this meant the quality of those loans would probably decrease, and, in turn, create a greater risk that some of them would result in losses. At the same time, executive pay was soaring, aided by stock options, which can encourage executives to take on greater risk.

For my 1,000-page report on the entire banking industry, with detailed reports of 47 banks, I wasn't just going to go negative on a few main stocks but the entire sector. This was completely the opposite of what most analysts were saying, not just about banks but about all sectors.

In decades past, the ratio of buy ratings to sell ratings had not been this lopsided, and in theory it should be roughly 50-50. That seems right, doesn't it? Some stocks go up, some go down, because of the overall market direction or competitive threats or issues specific to each company. In the late 1990s, though, the ratio was 100 buys or more for every sell. Merrill Lynch had buy ratings on 940 stocks and sell ratings on just 7. Salomon Smith Barney: 856 buy ratings, 4 sells. Morgan Stanley Dean Witter: 670 buys and exactly 0 sells.

Analysts almost never said to sell specific companies, because that would alienate those firms, which then might move business for bond offerings, equity deals, acquisitions, buybacks or other activity away from the analyst's brokerage firm. Say the word "sell" enough times, and you win a long, awkward elevator ride out of the building with your soon-to-be-former boss. And here I was, ready to go negative on the entire banking sector.

At the company's morning meeting between analysts and the sales staff, I gave a short presentation on the report. "In no uncertain terms," I said, "sell bank stocks. I'm downgrading the group. Sell Bank One, sell Chase Manhattan…." The message went out over the "hoot," or microphone, to more than 50 salespeople around the world. They would relay my thoughts to more than 300 money managers at some of the largest institutional investment firms in the business.

Afterward, I went back to my desk. Safe so far, I thought, and picked up the phone to call some of the biggest banks that had been downgraded, to give them a heads-up, along with some of the firm's institutional-investing clients. Not long after that, I was summoned back to the hoot for a special presentation to the sales force, something that had never happened before. They wanted me to clarify my thinking. Why not just leave the ratings at hold?

I laid out my case again: declining loan quality, excess executive compensation and headwinds for the industry after five years of major growth driven by mergers.

The counterattack started almost immediately. One portfolio manager said, "What's he trying to prove? Don't you know you only put a sell on a dog?" Another yelled, "I can't believe Mayo's doing this. He must be self-destructing!" One trader at a firm that owned a portfolio full of bank shares—which immediately began falling—printed out my photo and stuck it to her bulletin board with the word "WANTED" scribbled over it. I'd poked a stick into a hornets' nest.

That morning, I got a call from a client who runs a major endowment. "Check out the TV," he said. On CNBC, the commentators had picked up on the news and were now mocking me. Joe Kernen joked: "Who's Mike Mayo, and do we know whether he was turned down for a car loan?" I even got an ominous, anonymous voice mail from someone with a strong drawl cautioning, "Be careful with what you say."

Of course, the banks that I had downgraded were even more furious, and they let me know it. Routine meetings with management are a standard part of my work, yet when I requested these meetings after my call, several banks said no. Worse, a couple of big institutions in the Midwest and Southeast threatened to cut all ties with Credit Suisse—no more investment banking deals, no more fees.

Within a few months, the market began to experience problems. The Standard & Poor's bank index peaked in July 1999 and fell more than 20% by the end of the year. Regional banks, in particular, had their worst performance compared to the overall market in half a century.

***

I was still negative on the sector in 2001, when I moved over to Prudential, and I initiated my coverage with nine sell ratings. This was a tough stance to take at the time because bank stocks were on the rise. Soon enough, I would run into more of the usual problems.

---

Related story:

2 Comments

2 Comments

Reader Comments (2)

Hey, everyone, I got news for ya--NOTHING in this universe, and not even the universe itself, shows infinite growth. Nothing. Think about that when you dump you hard-earned $$$ into the black hole of a ponzi market. And to people you have never, nor will ever meet...insanity...