The Daily Bail

RIP Journalism: A Post Mortem...

Feeds: Email, RSS & Twitter

Most Recent Comments

- February 7 - Flynn Michael on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- February 7 - Flynn Michael on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- November 25 - ross smith on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- October 23 - PDQ Bail Bonds on PUT DOWN THE FLAME: Gen. Petraeus Speaks Out On Quran Burning: Freedom Of Speech Vs. Troop Safety

- October 23 - PDQ Bail Bonds on CHART SHOCK: Consumer Debt To GDP -- 'UGLY' Would Be An Understatement -- Much More Deleveraging Ahead

- October 20 - Sawan Merwat on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- August 14 - Thomas on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- June 5 - Top 5 online casinos on Dylan Thomas Jefferson: "Banks Have Taken Over The Government And Made Taxpayers Slaves To Bank-Run Gambling Casinos"

- June 5 - Casino bonuses on Dylan Thomas Jefferson: "Banks Have Taken Over The Government And Made Taxpayers Slaves To Bank-Run Gambling Casinos"

- March 8 - Renata on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- March 4 - Madagascar visa for Italy citizens on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- March 4 - Malagasy visa requirements for Italian citizens on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- March 4 - Malagasy visa requirements for Italian citizens on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- March 3 - Emergency Visa to Azerbaijan on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- March 1 - Jameson Clark on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 27 - Indian 30 Days Tourist eVisa on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 27 - Myanmar Tourist EVisa on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 26 - Kenya eTA for U.S Citizens on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 26 - apply for Saudi Arabia e Visa on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 26 - Sam Seeder on Bailout Films Presents | All The Plenary's Men

- February 25 - John Murley on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 25 - Egypt visa on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 25 - Charles on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 25 - Thomas on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 25 - Bahrain Visa online on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 25 - how to get visa for vietnam from india on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 25 - Robert on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 25 - John on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 25 - how to get visa for vietnam from india on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 25 - What is a Mexico Visa? on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 24 - Ethiopia Visa application form on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- February 24 - what can I do in Kenya with an eTA? on Dow Turns NEGATIVE After Fed Statement, Losing 200 Points - Full Text Of FOMC Statement

- November 21 - John on Bailout Films Presents | All The Plenary's Men

- October 11 - Data Science Training on HOLY CURRENCY: Bitcoin Up 1500% In 9 Months!

- June 18 - KetoCore ACV Gummies on Demand To See Your Mortgage Note! -- Brand New Website Makes It Simple

- March 21 - Bangalore Medical College and Research Institutei on It Takes a Pillage: Behind the Bonuses, Bailouts, And Backroom Deals From Washington To Wall Street

- March 21 - Bangalore Medical College and Research Institute on It Takes a Pillage: Behind the Bonuses, Bailouts, And Backroom Deals From Washington To Wall Street

- December 26 - Altitec on SUNE SETS: SunEdison Files For Bankruptcy

- December 23 - Kailash Deepak Hospital on Bailout AIG: Joseph J. Cassano Is An Irresponsible Asswipe Who Deserves To Spend The Rest Of His Days In Federal Prison

- December 14 - Heritage Solar on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- December 12 - VIP Bail Bonds on PUT DOWN THE FLAME: Gen. Petraeus Speaks Out On Quran Burning: Freedom Of Speech Vs. Troop Safety

- October 18 - karen perry on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- October 14 - Digitize1989 on The Mafia Is Moving Into Green Energy

- September 22 - Altitec on SUNE SETS: SunEdison Files For Bankruptcy

- September 22 - Altitec on SUNE SETS: SunEdison Files For Bankruptcy

- September 11 - karen perry on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- September 11 - karen perry on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- August 14 - karen perry on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- August 14 - GARVAN MAIREAD on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- June 23 - Hasan Ali on S&P Downgrades Irish Debt On Concern Over Cost Of Bank Bailouts, Outlook Negative

- February 9 - Joshua on The Founding Fathers: Smugglers, Tax Evaders And Traitors

- January 23 - karen perry on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- September 28 - May Gary on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- September 20 - May Gary on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- August 10 - GARVAN MAIREAD on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- May 7 - scott james on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- April 27 - Messi on Protesters Set Fire To KFC & Hardees In Tripoli (PHOTOS)

- March 14 - Rahul Singh on Fiscal Cliff Threatens 277,000 Federal Jobs (14% Of Total)

- February 4 - Horst Danzmann on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- December 7 - The CBD Magazine on Where The Fuck You Been?

- December 2 - anijohnson on Where The Fuck You Been?

- October 23 - Elvis Roberts on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

- October 14 - Евгений on HOLY CURRENCY: Bitcoin Up 1500% In 9 Months!

- August 21 - Michael B on Anti-Bailout Motivation From Coach Bob Knight: "I'm Tired Of This Shit; This Is Absolute F***ing Bullshit."

- July 30 - ray on Trump Won't Appoint Special Prosecutor In Clinton Case

- July 29 - <a href="https://www.vapeciga.com/collections/vapo on It Takes a Pillage: Behind the Bonuses, Bailouts, And Backroom Deals From Washington To Wall Street

- July 17 - Johnson on Black Friday Shopping In Post Apocalyptic America

- July 6 - Play Casino on Dylan Thomas Jefferson: "Banks Have Taken Over The Government And Made Taxpayers Slaves To Bank-Run Gambling Casinos"

- July 6 - Play Casino on Dylan Thomas Jefferson: "Banks Have Taken Over The Government And Made Taxpayers Slaves To Bank-Run Gambling Casinos"

- March 27 - John Tim on SunEdison: The Biggest Corporate Implosion In U.S. Solar History

Cartoons & Photos

SEARCH

13 Comments

13 Comments{kind=link}

Copyright © 2009-2016 DailyBail. All rights reserved.

Reader Comments (13)

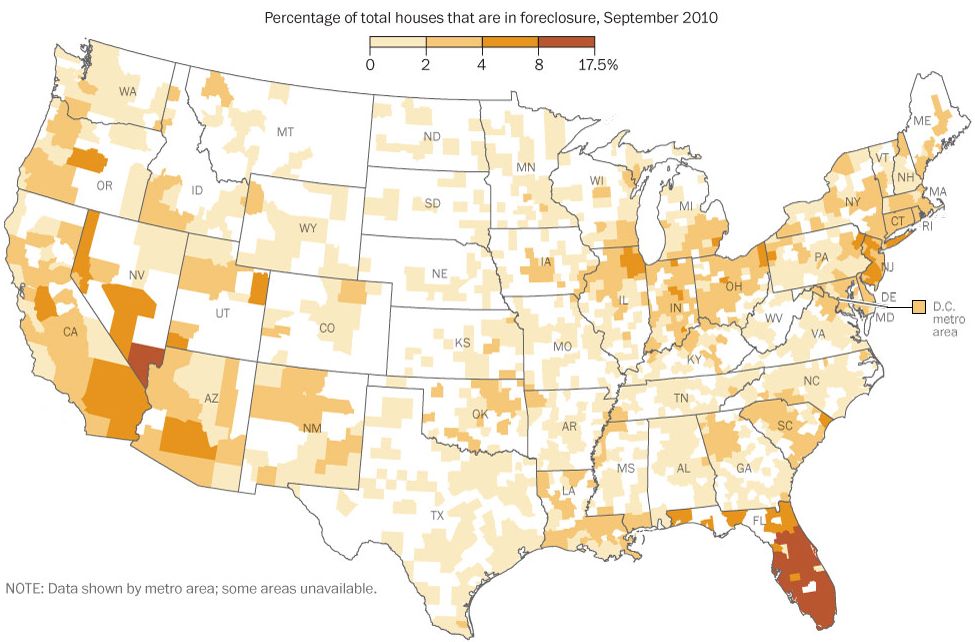

source for the map...

http://globalresearch.ca/index.php?context=va&aid=22283

Daley is personally opposed to the creation of Warren's brainchild, the CFPB, sources said, although he's in support of better regulation for the financial sector.

http://www.youtube.com/watch?v=wN0rcNJXFfI

DB, I don't know about JPM getting squeezed in silver... I certainly hope so. But for the last few days the price just couldn't cross $31, and then today... Whammo! $31.80, seemingly for no reason at all.

http://www.reuters.com/article/2012/06/08/us-usa-housing-blight-idUSBRE85707320120608

[snip]

The vacant home was foreclosed on in August 2011 by Bank of America, which has done nothing to repair it.

And in a cruel twist that underscores the connection between the housing meltdown and the fiscal crisis afflicting many local governments, the city of Los Angeles lacks the wherewithal to force the property owner to clean up the mess.

Across America, bank-owned, blighted houses sit untouched, sometimes for years, disfiguring what in many cases are already troubled neighborhoods. Activists say the problem is particularly acute in minority areas. And many cities do not have the resources, the will or the power to force banks to maintain their properties.

http://www.counterpunch.org/2012/09/04/obamas-secret-plan-to-prop-up-housing-prices/

[snip]

Private Equity firms are piling in to the housing market to take advantage of bargain basement prices on distressed inventory. The Obama administration is stealthily selling homes to big investors who are required to sign non-disclosure agreements to ensure that the public remains in the dark as to the magnitude of the giveaway. Aside from the steep discounts on the homes themselves, the government is also providing “synthetic financing to reduce the up-front capital required if they agree to form a joint venture with Fannie Mae and share proceeds from the rental or sale of properties.” (Businessweek)

In other words, US-taxpayers are providing extravagant financing for deep-pocket speculators who want to reduce their risk while maximizing their profits via additional leverage. The plan resembles Treasury Secretary Timothy Geithner’s Public-Private Partnership Investment Program, (PPIP) which Columbia University professor Joseph Stiglitz denounced in an op-ed in the New York Times. Here’s what he said:

“The Obama administration’s $500 billion or more proposal to deal with America’s ailing banks has been described by some in the financial markets as a win-win-win proposal. Actually, it is a win-win-lose proposal: the banks win, investors win — and taxpayers lose.”

The same rule applies here. Speculators are getting lavish incentives (gov financing, low rates, and severe discounts) in secret deals to buy distressed inventory which should be available to the public at market prices. If that’s not a ripoff, then what is?

http://www.reuters.com/article/2012/09/05/us-rescap-bankruptcy-idUSBRE88408720120905

[snip]

Mortgage lender Residential Capital RESC.UL is poised to reap billions in a bankruptcy auction of its assets next month - an unusual turn for a subprime lender in Chapter 11.

http://sweetness-light.com/archive/hillary-clinton-foreclosures-and-whitewater

“What this crisis is at bottom is a total loss of trust,” Senator Hillary Clinton told Joe Scarborough and Mika Brzezinski on the MSNBC Morning Joe show Tuesday. “People don’t believe what they are being told, Americans have no reason to believe either their government or the Wall Street banks…”

“Human nature being what it is, people are going to test the limits,” of any system, she indicated, which is what we have seen. “Let’s get together, recognize that we need new frameworks that keep people from abusing either the public trust or the private trust.” …

These and similar pronouncements from the Clintons about protecting “the little guy” have brought to mind some excerpts we posted back in January from Peter Schweizer’s (oh so aptly titled) book, Do As I Say (Not As I Do), pp 106-109:

Do As I Say (Not As I Do)

… Then consider the Whitewater investment. Forget for a minute about all the scandal associated with the word and the convoluted financing arrangements. Look at it for a minute as a pure investment—the biggest business venture that the Clintons had ever been involved in prior to the presidency.

Back in 1978, Bill Clinton was a popular Arkansas attorney general running for governor. He was campaigning as a reformer, an advocate of “consumer protection” and “rights for the elderly.” Like Hillary, he was concerned about unscrupulous “private corporations.” And as he has so often done in his public career, he made a point of claiming the moral high ground over his opponent.

An old friend and political operative, Jim McDougall, came to Bill and Hillary with an investment idea. He wanted to purchase 230 acres of land situated along the White River in the Ozark Mountains of north Arkansas and subdivide it to sell lots as vacation sites. McDougall promised huge returns, on the order of 20 percent a year. The Clintons thought it sounded like a great plan. Hillary in particular had high hopes for the property. While publicly criticizing Ronald Reagan’s tax cuts, she wrote McDougall in 1981: “If Reaganomics works at all, Whitewater could become the western hemisphere’s Mecca.”

The Clintons put no money into the investment. But Hillary, as an attorney in private practice, played an important role in establishing and running the venture. And what a venture it was meant to be. Whitewater was not designed as a regular real estate company. The plan was to sell lots, mainly to elderly retirees and middle-class families, by advertising in small-town newspapers. (They advertised several times in Mother Earth News.) Ordinarily, of course, when you buy a piece of land and finance the purchase, you receive a copy of the deed. If you start missing payments and can’t work things out with the finance company, they will eventually repossess the property. After paying off fees and debts, you will get back any remaining equity.

But the Clintons and McDougall did things differently. When customers wanted to buy a lot, they signed a simple purchase agreement. But this was no ordinary real estate contract. The small print at the bottom read: “In the event the default continues for 30 days … payments made by the purchaser shall be considered as rent for the use of the premises.” In other words, the buyers did not actually take ownership of their property until the final payment was made. If a buyer missed just one monthly payment, all their previous payments would be classified as rent and they would have no equity in the land at all.

This sort of contract was illegal in many other states, because it was considered exploitative of the poor and uneducated!’ One look at the experience of those who bought into Whitewater and you can see why.

Clyde Soapes was a grain-elevator operator from Texas who heard about the lots in early 1980 and jumped at the chance to invest. He put $3,000 down and began making payments of $244.69 per month. He made thirty-five payments in all—totaling $11,564.15, just short of the $14,000 price for the lot. Then he suddenly fell ill with diabetes and missed a payment, then two. The Clintons informed him that he had lost the land and all of his money. There was no court proceeding or compensation. Months later they resold his property to a couple from Nevada for $16,500. After they too missed a payment, the Clintons resold it yet again.

Soapes and the couple from Nevada were not alone. More than half of the people who bought lots in Whitewater—teachers, farmers, laborers, and retirees—made payments, missed one or two, and then lost their land without getting a dime of their equity back. According to Whitewater records, at least sixteen different buyers paid more than $50,000 and never received a property deed. The Clintons continued this approach up until the 1992 election, when they tried to quietly get out of the investment.

I say “the Clintons” did these things because Hillary was at the center of it all. Monthly payment checks were sent to the Whitewater Development Corporation in care of Hillary Rodham Clinton. In 1982, Hillary herself sold a home to Hillman Logan, who went bankrupt and then died. She took possession of the home and resold it to another buyer for $20,000. No one was compensated (and she didn’t report the sale on her tax return).

Hillary has always very indignantly maintained that she and her husband “did nothing wrong” with regard to Whitewater. After all, they lost money in the deal. But they have always avoided discussions about how the business was structured, and how it exploited the very people they have often professed to help. In the meantime, Sen. Hillary Clinton has gone on to champion the cause of going after banks and other lenders for “predatory mortgage lending practices.” In an amazing feat of moral dexterity, she cosponsored the Predatory Consumer Lending Act, claiming that mortgage fees are too high. (No, the law does not outlaw the type of financing scheme she was involved in.) …

Bear all this in mind when you hear Hillary shedding her crocodile tears about predatory lenders and unfair mortgage foreclosures.