Tuesday

Nov082011

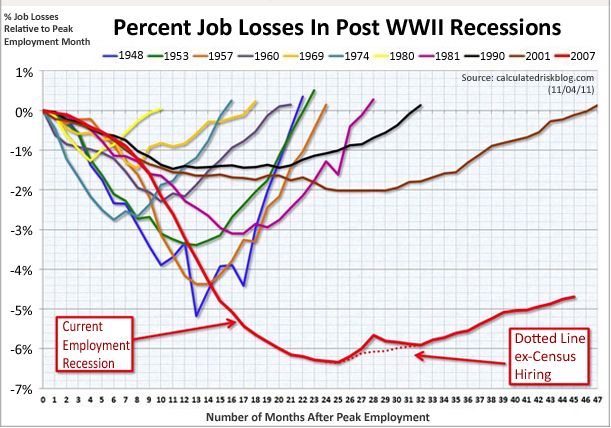

CHART OF THE DAY - The Scariest Jobs Chart Ever

This is what happens after a 20-year debt bubble fueled by two irresponsible Fed Chairman and their insatiable love for low interest rates.

A comparison of every post-WWII recession, and look at the progression of job losses from the beginning, down to the trough, and then through the comeback. As you can see, this recession hasn't been like any other.

7 Comments

7 Comments

Reader Comments (7)

Target credit card charges 22.90 percent interest, do you call that a low interest rate?

I was referring to endlessly low interest rates for home mortgages that fueled the housing bubble. Sorry for not being more clear.

http://swarmthebanks.blogspot.com/2011/11/why-did-pension-fund-managers-invest.html

These kinds of graphs are a bit misleading because they make it look like this range is a 1 to 100 range when it is actually a zoomed in range designed to exaggerate differences exponentially. Just sayin.

Why do you stand for interest being charged on money, at all?

If you knew what money is, interest would tick you off. It's how the powers that be, be.

However, interest rates ARE KILLING everybody but the ultra rich and causing everybody to go for the most profitable venture, even if it hurtles the world even faster to the end as we presently know it.

As for the comment about it being my fault because I am not on the streets protesting, I would suggest that I have been protesting since 2006 and have 10 banking watchdog blogs, plus 2 websites highlighting credit card fraud and usury destruction of the economy, plus another four or five political watchdog blog as well.

Here is a rundown of my various blogs and websites in the approximate order they were created.

www.shareamillion.com around 2006. I was asking for a temporary one million dollar loan for four or five years simply so I could use the interest on that amount for five straight years to provide my income so that I could begin my consumer advocacy work. I would never touch the principle. After five years I would offer the person their money back plus the possibility of taking all the data that was created and turning it into a book or documentary.

No one responded, and ironically, since I created that website in 2006, homeowners have lost 7.3 trillion dollars in home equity. My concerns were validated. Although I can't claim I could have stopped what happened from happening, my instincts were correct that things were going to get worse.

I went ahead and did my blogging as mentioned below anyways, but with no funding.

www.credit-card-cap.com (In 2007 I was advocating credit card interest rate reductions for those who are paying down their debts otherwise our economy would implode even more than it had at that point).

www.credit-protector.com (2007, exposes the tens of billions of dollars credit card companies have stolen from customers via their credit protector insurance programs.)

2008 was devoted to exposing various political frauds involving the democratic nomination process, blogs included www.hillary-wins.com, www.dailypuma.com, www.caucuscheating.com, www.florida-michigan.com, www.fair-reflection.com, www.mythirdparty.com (advocating a viable third party).

www.daily-protest.com (Created in April of 2009, protest against Chase Bank credit card practices,)

www.bloggersagainstchasebank.com (2009, unite bloggers who were unhappy with Chase Bank practices)

www.wallstreetchange.com (2009, offering practical ideas and solutions to both help the economy while hopefully stopping wall street from economically destroying the world's economy)

www.thecatwhoatechasebank.com (2009, a book devoted to Chase Bank atrocities, the job was too big to tail).

www.robotsagainstchase.com (2009, videos from people who hate chase bank)

www.parallelforeclosure.com (2009, exposing how Chase Bank forecloses on homeowners who are applying for HAMP)

www.swarmthebanks.com (2010, dedicated to swarming the banks when they treat a homeowner unfairly, turned into a bank watchdog blog instead)

www.unfairforeclosures.com (2011) Chronicling unfair foreclosures, have not been able to keep it going on a regular basis because there was too much information to have to process.

www.bankprotests.com (2011) Chronicling bank protests.

www.occupynews.net (2011) networking together 175 occupy blogs that have RSS feeds.

I was the guy protesting outside of various chase banks in the west san fernando valley back in April of 2009 warning everybody about the gloom that was to come.

I now have a solution based on all of the unpaid research work I have done. Allow the 99% to restructure their debts without being forced into a default first. It's a trillion dollar idea that would save homeowners from the clutches of the very entities that have caused them to need their debt restructured in the first place.

I have not heard a single hammer fall or saw start up within earshot of the center of town in over 4 weeks. Maybe they want work done. But I don't think so. Most ALL the labor force has gone and the people with money are sitting tight. This is a town of liars and the confusion is great. No incomming radiation monitoring anywhere, even though incredibly high rates were monitored and recorded close by a few months ago. If they can't see it, these overpaid TV flunkies don't believe it exists and refuse to react. They will wait the few years for their kids to come down with symptoms of the irreversible nature.