Backdoor bailout.

'Paulson and Geithner rolled AIG to bailout Goldman Sachs and other favored institutions.'

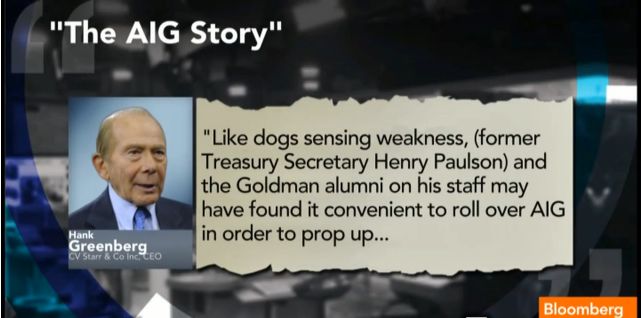

Start watching at the 3-minute mark. Excellent interview. He blames Eliot Spitzer for the start of AIG's problems, then discusses Geithner and Paulson.

Greenberg is the former Chairman of AIG. Broadcast Jan. 31, 2013.

***

WSJ Interview With Hank Greenberg

The former chairman of AIG wonders why Goldman Sachs got paid in full on its AIG exposure while AIG itself was forced into slow-motion liquidation.

How did it all come apart so quickly? Here are the pieces Mr. Greenberg says he sees falling into place. In 2005, a trade group called the International Swaps and Derivatives Association got together and drafted new standards for the kinds of credit default swaps AIG had been writing.

Previously, Mr. Greenberg explains, losses to the underlying securities were paid off at maturity. Now, cash payments would have to be forthcoming to cover any drop in value or credit downgrades even before any losses were realized.

"I don't know whether Goldman Sachs was the force behind the ISDA change or Deutsche Bank," Mr. Greenberg concedes. "That's something investigative reporters are going to have to spend time digging out."

The next piece fell into place, he says, with recent reports in the press about how, at the top of the housing bubble, "a couple of people there [at Goldman Sachs], bright guys, decide the housing market is going to collapse." Goldman went to work creating new subprime housing-backed derivatives , Mr. Greenberg says, and "began marketing the hell out of them and at the same time shorting them" (or betting they would fall in value).

Bingo. When the housing boom imploded, Goldman demanded giant cash collateral payments from AIG on a "mark to market" basis for housing-backed securities whose price was plummeting even if the underlying payment streams were intact. True, Goldman was hardly the only one demanding cash, but Mr. Greenberg is suspicious about the size of the payments Goldman demanded based on Goldman's own "marks" (i.e. estimate of the securities now-depressed value). "Goldman had the lowest marks on the Street by everything I hear," he says. "There was no exchange. Where was the price discovery? It was all in the eye of the beholder."

In short, it added up to a perfect trap for AIG. As panic spread through the financial sector, impossible amounts of cash were required of the firm under insurance contracts that had years to run and (as Mr. Greenberg argues and events seem to be showing) would likely end up performing adequately in the long run.

More on Spitzer and Greenberg. This is pretty funny:

Spitzer Battles Bartiromo Over AIG: 'You Are Under Oath Right Now Maria'