Why Paul Krugman, James Galbraith, Simon Johnson and John Hussman are right and Brad Delong, Tim Geithner and Lawrence Summers are clueless eunuchs. The issue is Treasury Secretary Geithner's solution to the banking crisis revealed this morning, which by the way falls entirely on you. Bank bondholders like Bill Gross are not even being asked to carry their own tampons.

The mother of all bailouts is really the mother of all uncloggings.

My argument with Brad Delong's thesis is simple. He doesn't give enough consideration to the probability that the price paid for bank assets will be too high. The entire plan is built upon non-recourse loans to the private sector. Bill Gross puts down 8% ( or is it 3% ), you and I put up the remaining 92%.

Sure, if things miraculously turn around, and asset prices rise, then the hedge funds and private equity cabals and Bill Gross get the shitload of the profits. That sucks.

However, it's much more likely that prices paid for the complex securitized will be too high and they will continue falling in value, and the taxpayer will get stuck with the substantial losses from the non-recourse loans. Delong's thesis seems to be (incorrectly according to krugman and many others) that these assets are actually UNDERVALUED currently by the market, and that fears about deterioration from here are killing the risk libido of potential private buyers. So all we need to do is incentivize the buyers to get horny again and the problem will be solved.

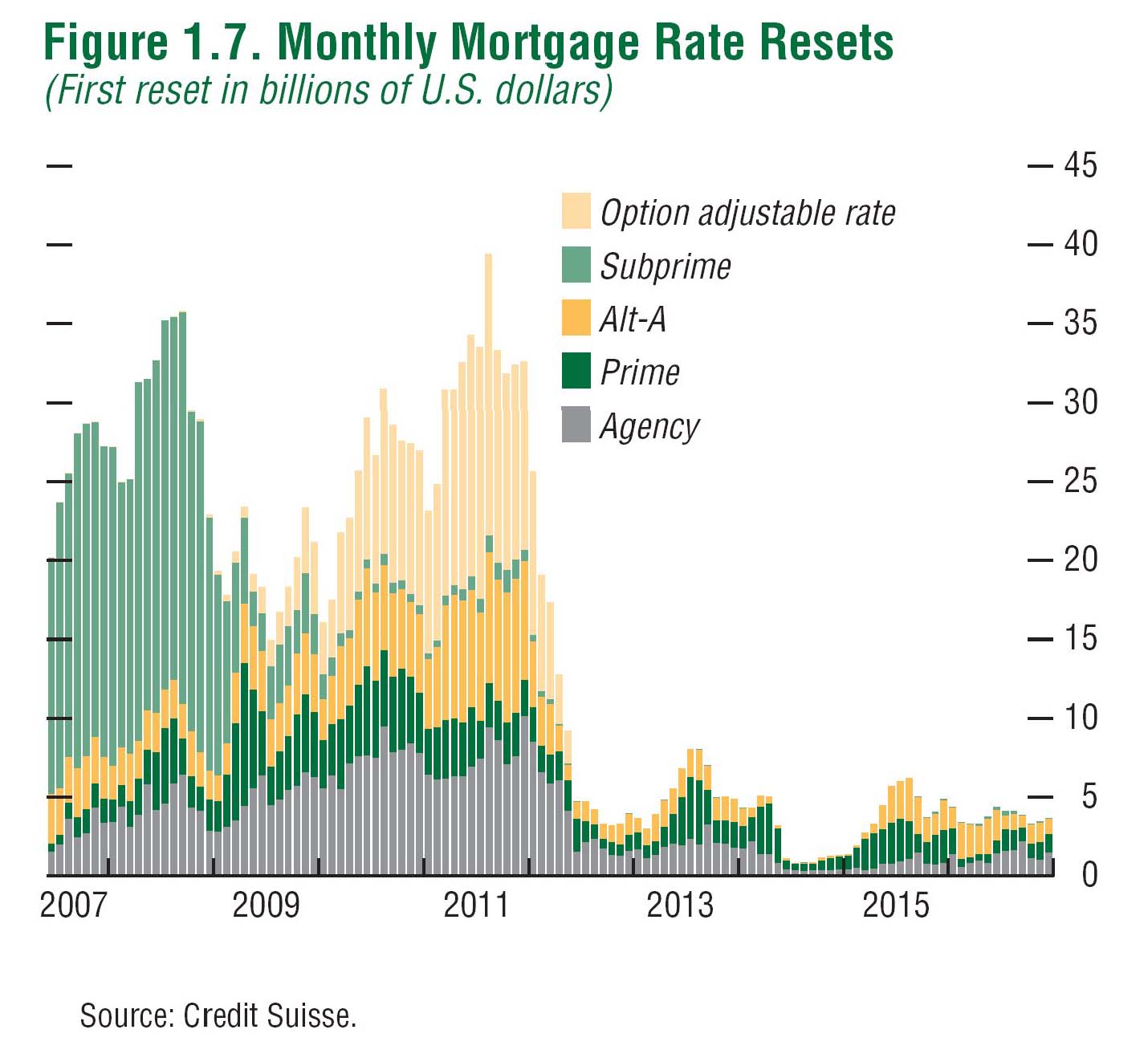

As stated above, I believe that these assets are likely fairly valued by the market. Or perhaps (shudder in panic) even overvalued. What? Overvalued at 25 cents? Yep. And here's why that is possible. The market has been WRONG with every bid so far. Every purchase of toxic shit over the last 12 months has been proven to be early. Every single one. And the housing problem is still getting worse. Take a look at this chart of mortgage resets still to come. Muy fea.

This is not a sub-prime problem anymore. It is an ALT-A and will soon be a prime and jumbo prime killer. Read Mr. Mortgage or Patrick.net daily and you will understand. Jingle mail and walk-aways are just gaining momentum. Many houseowners still cling to the grand illusion that prices will somehow start rising and they can get out whole. When the reality of their self-delusion is finally apparent, these price-arrogant debtors will give up hope and walk away.

A quick history lesson on the market's overvaluation of mortgage assets. Anyone else remember the UBS ALT-A firesale. Early last Summer, they sold a $25 billion portfolio of ALT-A junk at 64 cents on the dollar that was marked at 91 cents if memory serves. This was considered a desperate move at the time for UBS and a bargain for the buyer. Oh, but what do they say about time?

How's that buyer doing now? He's dead. Killed by the drop to 25 cents that those assets are currently worth. My point is that the market has been consistently WRONG on the value of these assets for 12 months. There has been an over-valuation of assets every step of the way down (how ya doin, Wilbur Ross?). Every single bid has proven to be too high, and there's little reason to believe today is any different.

So back to the Delong and Geithner fantasy.

Banks think 65 cents is fair value. Market says 25 cents. The Treasury's Geithner plan will maybe (big maybe) get bids up to 55 cents with taxpayer non-recourse loans. But with time 55 cents will prove to have been too high. When examined again in 12 months the value will be 25 cents or lower (for all the reasons I outlined above, principally because home prices have much further to fall). That's a 60% loss from a 55-cent purchase cost. Extra ouch for you and me.

All the losses on the non-recourse loans will be dumped onto the laps of hapless taxpayers. And what then? Nothing. Not a damn thing. Geithner and Obama will probably only get 1 shot at this fix, and they will have already busted their nut.

In summary taxpayers get little upside but all the downside. Bank bondholders absorb none of the risk or losses. Why do GM bondholders have to take 70% hits on their bonds but bank bondholders get to take the A-train and float with the hotties in first class ?

Political connections. And that is truly disgusting.

All bonholders of failed institusions should suffer. And for me it's a non-starter until bank bondholders are asked to bring their own Draino and join the unclog. We'll pay for the rubber gloves, the wetsuits and the kneepads but they have to get covered in shit like the rest of us.

Until then I will be always smiling but rarely happy.

DailyBail

DailyBail